Outsourcing AI Solutions in Finance: A Founder’s Playbook

Financial services firms spent $35 billion on AI in 2023, according to the World Economic Forum's 2025 report on AI in financial services. That number matters less as a bragging point than as a signal. AI in finance is no longer a side experiment owned by innovation teams. It's becoming part of how core operations run, how risk is controlled, and how finance leaders decide where to automate first.

That changes the outsourcing question.

Most founders don't need another article telling them AI is important. They need a practical way to buy it without creating a messy pilot, an unusable model, or a compliance problem nobody spotted during procurement. In finance, outsourcing AI solutions succeeds when the buyer treats the project as an operating model decision, not a software shopping exercise.

This playbook is built for that moment. It focuses on how to scope the work, what to ask vendors, which KPIs belong in the contract, how to structure a pilot, and where projects usually break.

The New Imperative for AI in Finance

In 2025, over 85% of financial firms are using AI for functions such as fraud detection and risk modeling, with spending projected to reach $97 billion by 2027. The generative AI segment alone is projected to grow from $1.95 billion in 2025 to $15.69 billion by 2034, according to RGP's 2025 AI in financial services research. That scale changes the conversation from “Should we try AI?” to “Which parts of finance should we outsource first, and under what controls?”

The practical implication is straightforward. If most serious firms are already applying AI somewhere in the stack, then waiting for perfect internal readiness becomes a competitive handicap. Outsourcing AI solutions in finance has become attractive because it lets a company access implementation capacity, domain knowledge, governance support, and integration talent without building every capability from scratch.

What has actually changed

The biggest shift is that finance teams are no longer outsourcing only labor-heavy back-office work. They're increasingly outsourcing the design and operation of AI-enabled workflows inside that work. That's a different category of engagement.

A founder evaluating this move should think in terms of embedded operational advantage:

- Faster execution: A specialist partner can usually move from use-case selection to pilot design faster than an internal team starting from zero.

- Stronger focus: Finance leaders can keep internal staff on approvals, exceptions, and judgment-heavy decisions instead of forcing them to become prompt engineers and ML operators.

- Better sequencing: Good partners know that invoice extraction, anomaly review, reconciliations, and compliance document handling need different controls and different success metrics.

For teams still mapping adoption maturity, AmasaTech's perspective on AI adoption in financial services is useful because it frames AI as an operating capability, not a novelty feature.

What this means for founders

Outsourcing doesn't remove responsibility. It changes where responsibility sits.

Practical rule: If an outsourced AI vendor can explain the model but can't explain the workflow, approvals, exception handling, and audit trail, they're not ready for finance.

That's why the strongest finance AI engagements start with a narrow business process, a controlled dataset, and a measurable operational outcome. Not with a broad promise to “transform finance.”

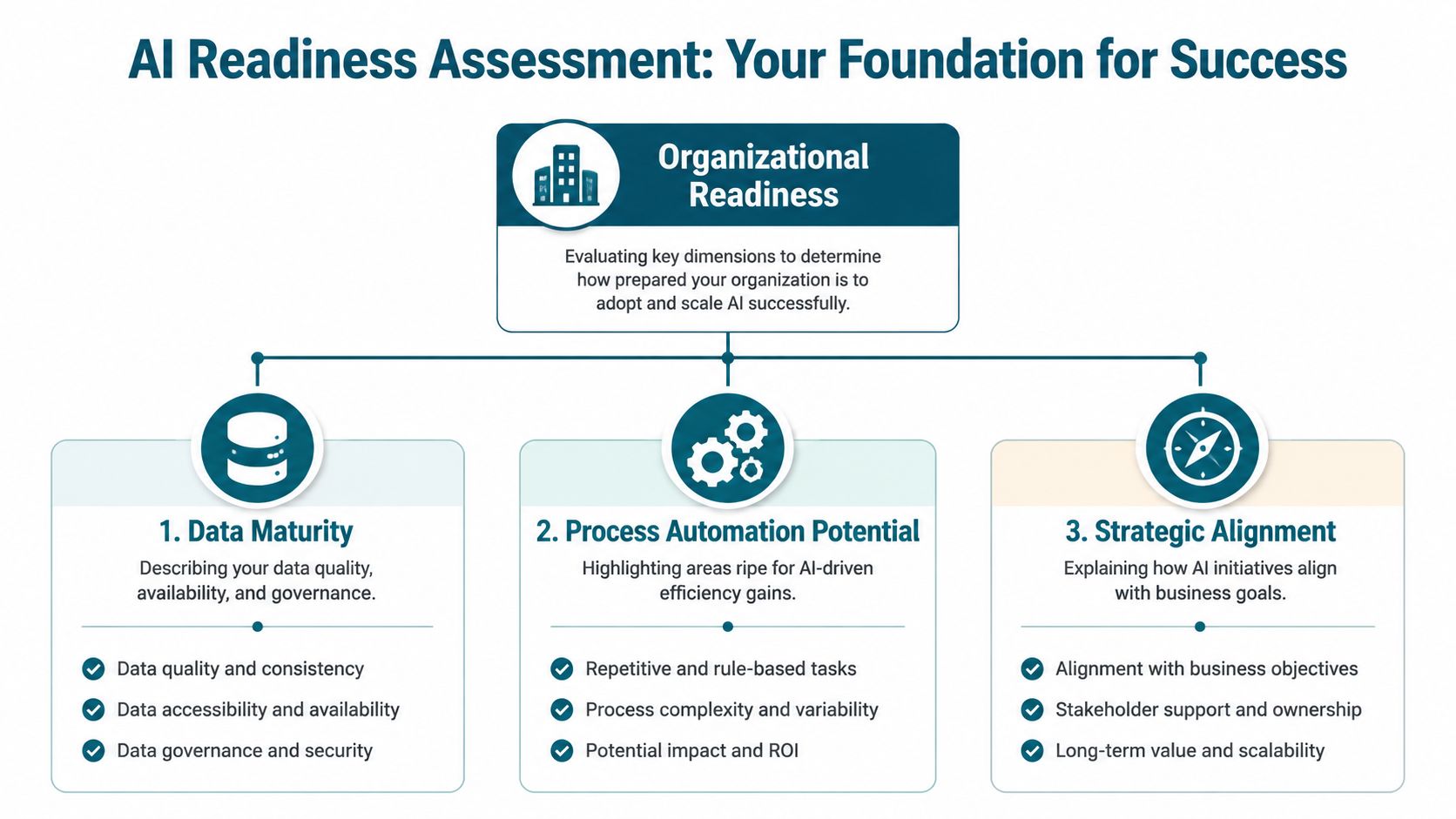

Assess Your Readiness and Identify High-Impact Use Cases

The safest first move is usually not customer-facing AI. The Financial Stability Board reports that AI adoption in financial services has accelerated, but most current use cases are concentrated in internal operations and regulatory compliance, with new-revenue use cases not yet widely observed. That's a useful benchmark because it points founders toward the highest-probability starting point.

Start with a blunt readiness check

Most failed AI outsourcing projects were weak before the vendor was ever hired. The process was inconsistent, the data was scattered, or nobody owned post-deployment decisions.

Use a simple three-part assessment before you issue an RFP:

Data maturity

- Source coverage: Are the needed records already stored in systems your vendor can access through APIs, exports, or secure batch transfers?

- Data quality: Do key fields have missing values, duplicate records, inconsistent naming, or document-format variation?

- Governance: Is there a named owner for each dataset used in training, testing, and production review?

Process automation potential

- Repetition: Does the task happen often enough to justify workflow setup, review logic, and monitoring?

- Rules plus judgment: Is there a stable baseline process with clear exceptions, or is every case handled differently by different analysts?

- Downstream action: Can the model's output trigger a useful next step such as flagging, routing, reconciling, or drafting?

Strategic alignment

- Business pain: Is the use case tied to cost, cycle time, quality, compliance, or working capital?

- Executive sponsor: Will a finance leader approve process changes when the pilot exposes broken handoffs?

- Change tolerance: Can the team absorb a new workflow now, or are they already mid-migration on ERP or reporting systems?

If you want a structured internal worksheet before vendor outreach, this AI readiness checklist is a good framing tool.

Choose use cases by operational risk

Not all finance AI projects deserve equal priority. A practical ranking looks like this:

| Use case category | Good first project | Why it works |

|---|---|---|

| Low risk and high control | Document intelligence for KYC or KYB packs, policy review, invoice classification | Clear inputs, reviewable outputs, strong auditability |

| Moderate complexity | Compliance monitoring, anomaly detection in internal transactions, reconciliation support | Valuable, but needs clear escalation paths |

| High complexity | Customer-facing advice, autonomous credit decisions, trading-adjacent workflows | Higher model risk, more scrutiny, harder sign-off |

Start where the team can compare AI output against an existing manual baseline. That makes trust easier to build and errors easier to catch.

A bad first use case is one with unclear ownership, poor source data, and immediate external exposure. A good first use case is internal, repetitive, reviewable, and operationally painful enough that people will adopt a better workflow.

Define Success with Clear KPIs and a Detailed SOW

Most AI outsourcing failures can be traced back to one document. The statement of work was vague.

Traditional IT scopes often stop at deliverables like “build model,” “deploy dashboard,” or “integrate system.” That isn't enough for finance. An AI-specific SOW has to define the business task, the data boundaries, the review workflow, and the rules for what happens when the model is wrong.

What belongs in an AI SOW

A workable scope should include these components:

Business objective

Name the process in plain language. Example: classify incoming invoices, extract key fields, route exceptions, and prepare ERP-ready output for reviewer approval.In-scope inputs

Specify document types, systems of record, historical data sources, and what is excluded. If email attachments are included but handwritten scans are excluded, write that down.Expected outputs

Define fields, labels, confidence logic, exception categories, and required human review steps.Integration points

List the ERP, CRM, ticketing system, document repository, and notification channels involved. Say who owns each connector.Acceptance criteria

Don't stop at technical completion. Include operational acceptance, user acceptance, and rollback conditions.Governance and review cadence

Set weekly pilot reviews, escalation owners, audit-log requirements, and retraining or prompt-change approval rules.

KPI templates finance teams can actually use

Below are sample KPI structures that are useful because they connect model behavior to finance outcomes.

AP and invoice automation

- Cycle time per invoice: Measure time from receipt to routed output.

- Field extraction quality: Track correctness for required invoice fields during reviewed processing.

- Exception routing quality: Measure whether the right exceptions go to the right approvers.

- Manual touch rate: Track how often staff must fully rework a document instead of reviewing it.

Compliance monitoring

- Alert precision by rule family: Measure whether alerts are relevant enough for analysts to trust.

- Review turnaround time: Track how quickly flagged items move from detection to disposition.

- Escalation quality: Measure whether higher-risk cases are routed correctly.

- Audit trace completeness: Confirm every decision is explainable and reviewable.

Financial forecasting support

- Forecast accuracy versus actuals: Compare model-assisted forecasts with realized outcomes.

- Analyst effort saved: Track reduction in manual spreadsheet assembly and data preparation.

- Scenario turnaround time: Measure how quickly the team can produce revised scenarios after an input change.

- Variance explanation coverage: Assess whether generated explanations are useful enough for analyst review.

For teams building internal operating discipline around these measures, this guide to AI transformation progress monitoring is a practical complement.

A good SOW makes disagreement visible early. A bad one hides disagreement until after deployment.

Vet Vendors for Finance Expertise and Security

A polished demo does not tell you whether a vendor can survive a quarter-end close, an internal audit, or a regulator request. In finance, the ultimate test is operational discipline. Can the team explain why the model made a recommendation, show who approved a rule change, and contain access to sensitive data without slowing the business down?

I have seen finance teams choose a vendor based on model accuracy claims, then spend months fixing weak controls, unclear ownership, and poor exception handling. The expensive mistake is not hiring a weak data science team. It is hiring a team that cannot operate inside finance controls.

What to ask beyond the demo

Treat vendor diligence like a control review with technical validation attached. Ask for evidence, not positioning.

Use a checklist like this:

- Finance workflow experience: Ask which finance processes they have put into production, what approval steps were required, and where human review sits for exceptions, overrides, and final sign-off.

- Security controls: Ask how they handle encryption, key management, tenant isolation, role-based access, audit logs, retention schedules, and incident response. Confirm whether they can work inside your cloud, your region, and your compliance requirements.

- Change management: Ask who can change prompts, rules, thresholds, and models in production. A credible answer includes approvals, testing steps, rollback procedures, and a record of every change.

- Production support: Ask what happens when source documents change format, an upstream system changes a field, or output quality drops over time. You want operating procedures, not reassurance.

- Integration ownership: Ask who maintains connectors, how version changes are tested, and who is accountable when ERP, CRM, or document management systems break the workflow.

A useful benchmark is whether the vendor can describe the full operating flow, from ingestion to reviewer queue to audit trail. This KYB automation case for a fintech leader shows the level of workflow detail buyers should expect in a regulated environment.

Artifacts to request before you shortlist

Do not rely on a capabilities deck alone. Ask each vendor to provide the same small set of artifacts so you can compare them side by side.

| Artifact | What to look for |

|---|---|

| Sample architecture diagram | Data flow, model boundary, storage locations, security controls, system dependencies |

| Redacted audit log or decision trace | User actions, model output history, timestamped approvals, retained evidence |

| Incident response summary | Severity levels, escalation path, response times, customer notification process |

| Change control example | Approval record for a prompt, rule, or threshold update with rollback steps |

| Production support plan | Named owners, monitoring coverage, issue triage, maintenance windows |

Sample vetting questions for the buying team

Ask, “Show us how a production change is approved, tested, and rolled back,” before you ask, “How accurate is the model?”

Add these questions to your shortlist process:

| Question | What a strong answer includes |

|---|---|

| Who owns model changes in production? | Named approval workflow, change log, rollback path |

| How is output reviewed? | Confidence thresholds, exception routing, human review design |

| How do you support audits? | Version history, traceable decisions, retained evidence |

| What breaks the system fastest? | Direct discussion of source-data drift, template changes, and process variation |

| What security controls are customer-configurable? | Clear boundaries between vendor-managed and client-managed controls |

If a vendor avoids these questions, or keeps steering the discussion back to generic automation claims, remove them from the process. In finance, weak controls erase ROI fast.

Design Pilots and Choose Your Procurement Model

The 2025 ISG Provider Lens announcement on finance and accounting outsourcing notes that providers' use of AI, GenAI, and advanced analytics has shifted from pilots and proofs of concept into production environments, including anomaly detection, reconciliations, and cash flow forecasting. That matters because procurement has to catch up. If AI is moving into core operations, then contracts should reflect outcomes, controls, and production support, not just build effort.

A sample 90-day pilot structure

A pilot should be narrow enough to finish and broad enough to prove operational value. A good example is client onboarding document intelligence for KYB or entity verification.

Days 1 to 15

- Define document types in scope

- Confirm source systems and secure access method

- Freeze pilot KPIs

- Build exception taxonomy

- Name decision owners on the finance or compliance side

Days 16 to 45

- Prepare sample dataset

- Configure extraction, classification, and routing logic

- Test against historical records

- Review edge cases with operations staff

- Adjust review thresholds and workflow rules

Days 46 to 75

- Run the model in shadow mode beside the current process

- Compare AI output to analyst-reviewed output

- Measure exception categories and reviewer effort

- Fix integration gaps before live routing starts

Days 76 to 90

- Start limited live deployment

- Review KPI performance weekly

- Decide go, revise, or stop

- Document production requirements for phase two

For teams evaluating document-heavy finance workflows, this example on invoice OCR and AI is directionally helpful because it shows how narrow process automation can create a reliable first win.

Procurement models compared

The procurement model affects behavior. A fixed-price build can work for a tightly defined pilot. It often breaks down when requirements evolve after exposure to real finance data. Outcome-based structures usually fit better once the workflow and KPIs are clear.

| Dimension | Fixed-Price Project | Outcome-as-a-Service |

|---|---|---|

| Scope definition | Best when scope is narrow and stable | Better when workflow will mature through live use |

| Risk allocation | Buyer carries more risk if assumptions were wrong | Vendor shares more delivery risk tied to outcomes |

| Change handling | Scope change often triggers renegotiation | More flexible if outcome definition is stable |

| Incentive alignment | Rewards delivery of agreed tasks | Rewards sustained business performance |

| Best fit | Early pilot with contained variables | Production deployment tied to operational KPIs |

If you can't define the operational outcome, don't sign an outcome-based contract yet. Use a pilot to establish the baseline first.

A common mistake is choosing fixed price because it feels safer, then discovering the work is in exception handling, data cleanup, and integration changes that were excluded from scope.

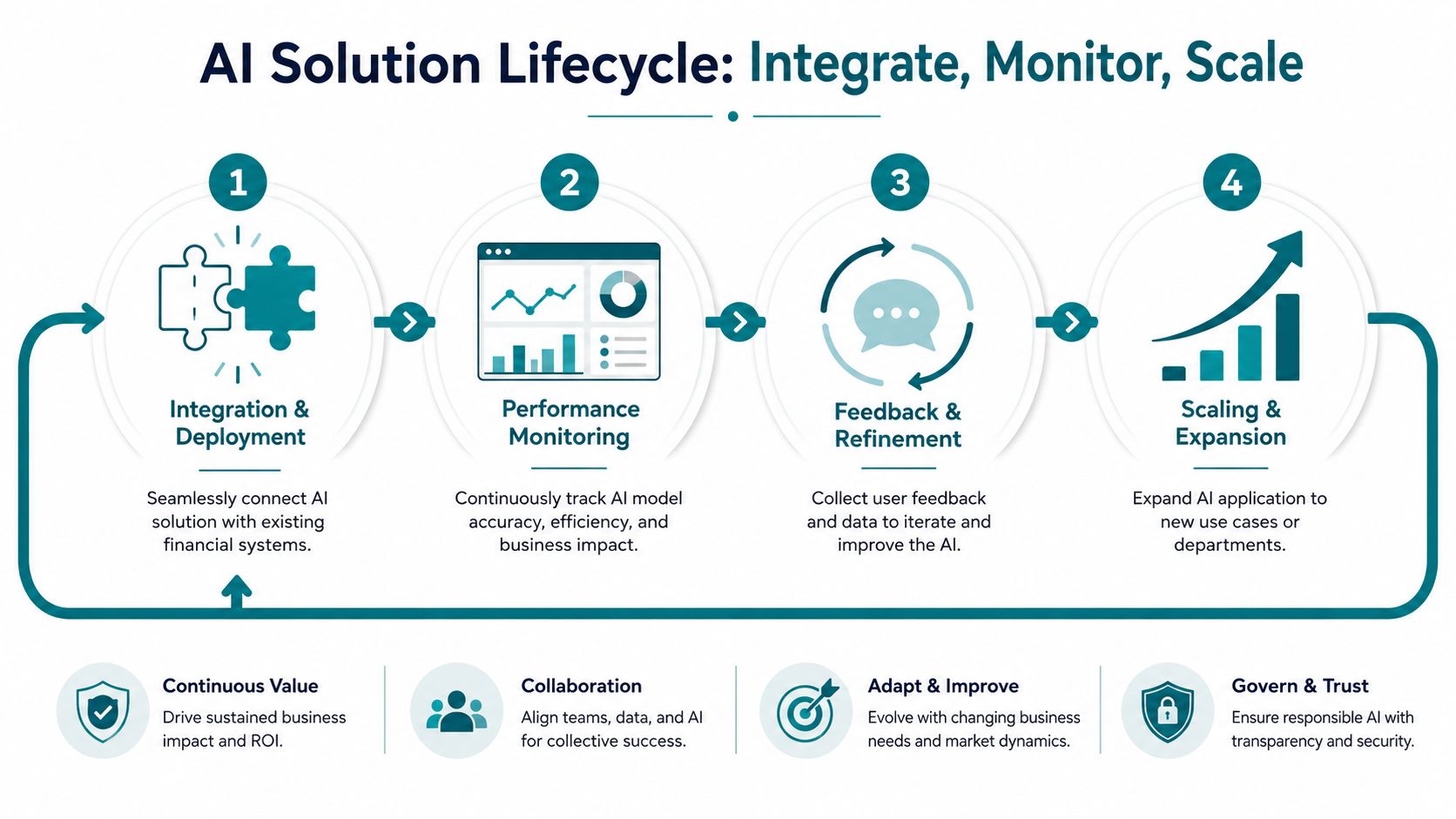

Integrate Monitor and Scale Your AI Solution

Once the contract is signed, most of the hard work begins. In finance, the biggest hurdle usually isn't model building. Industry analysis shows the harder problem is integrating with fragmented systems and solving data-readiness issues, with value primarily coming from data reconciliation and workflow integration first, as discussed in Insight Partners' analysis of AI and the financial services data problem.

Integration work that buyers underestimate

Teams often imagine deployment as “connect model to system.” In practice, finance integration usually involves five separate workstreams:

- Data normalization: Standardize field names, formats, currencies, document types, and reference tables across systems.

- Workflow redesign: Decide what happens after prediction or extraction. Who reviews it, who approves it, and what triggers escalation?

- System connectivity: Connect the AI layer to ERP, CRM, document stores, inboxes, or case management systems.

- Control design: Add logs, confidence thresholds, review queues, and exception handling.

- Operational fallback: Define what the team does when the model can't classify, extract, or route confidently.

Monitoring after go-live

The right post-launch dashboard isn't only about model accuracy. Finance leaders need a mixed scorecard that includes process and business indicators.

Track at least these categories:

| Monitoring area | What to watch |

|---|---|

| Output quality | Review error patterns, recurring exceptions, and confidence distribution |

| Workflow health | Queue volume, stuck items, approval lag, failed handoffs |

| Data integrity | Missing inputs, template changes, format drift, duplicate records |

| Business impact | Cycle time, reviewer effort, rework burden, control quality |

The first production month usually teaches you more about process design than model design.

How to get the team to trust it

Adoption fails when staff believe the AI is either replacing judgment or creating hidden rework. Fix that early.

Train reviewers on three things only:

- What the system is allowed to decide

- What still requires human approval

- How to flag bad outputs so the workflow improves

That framing matters. Finance teams don't need a lecture on neural networks. They need a reliable review process, visible escalation rules, and evidence that feedback changes the system.

Implement Governance and Control Costs for Long-Term Success

Finance leaders sometimes treat outsourced AI as a completed purchase once the workflow goes live. That's the wrong mental model. A live AI process behaves more like an operating capability than a software license. It needs ownership, review, and cost discipline.

A lightweight governance model works better than a bureaucratic one.

The governance layer that actually matters

Assign four standing owners:

- Business owner: Usually finance or operations. Owns KPIs and process changes.

- Data owner: Owns source quality, access, retention, and change notification.

- Risk or compliance owner: Reviews controls, auditability, and approval boundaries.

- Vendor lead: Owns support, issue triage, and improvement backlog.

Meet on a fixed cadence. Review output quality, workflow failures, business impact, and open risks. If the vendor can't support that level of operational review, they're selling a project, not a managed capability.

Cost control without slowing the project down

AI costs can drift when nobody watches usage patterns, model choice, exception volume, or reprocessing behavior. Good cost control is simple:

- Track usage by workflow: Don't lump all AI costs into one bucket.

- Separate pilot and production economics: A test environment often has very different usage patterns from a stable live workflow.

- Review exceptions as a cost driver: Rework and unnecessary human review can erase the value of automation.

- Set approval rules for scope expansion: Adding new document types, entities, or business units changes cost and risk.

The strongest outsourcing relationships in finance stop looking like vendor management after the first successful phase. They start to look like a joint operating model with shared accountability for outcomes, controls, and continuous improvement.

If you're planning your first serious move into outsourcing AI solutions in finance, AmasaTech can help you approach it the right way. The team works from AI audit to deployment and ongoing optimization, with outcome-based engagements tied to measurable KPIs so you can de-risk implementation and focus on finance workflows that deliver value.