Generative AI Solutions in Insurance: A Practical Guide

59% of insurance organizations have already adopted generative AI, and those using it report 61% gains in staff productivity, 56% cost savings, and 50% shorter customer call times, according to a 2024 industry report cited by Master of Code's insurance analysis. That changes the conversation.

Generative AI in insurance is no longer about whether the technology has potential. The key question is how to deploy it in a way that survives underwriting scrutiny, claims realities, security review, and executive budget approval. Most insurers don't need more brainstormed use cases. They need a path from pilot to production that ties AI to handling time, decision quality, service performance, and governance.

Insurance is a strong fit for generative AI because the work is dense with documents, emails, notes, forms, policies, endorsements, and exception handling. But that same complexity is why careless deployments fail. Generic chatbots sound impressive in demos and create problems in live operations. Grounded systems tied to approved content, workflow checkpoints, and human review tend to create durable value.

The Tipping Point for Generative AI in Insurance

The insurance industry has crossed the threshold where generative AI is a strategic operating issue, not an innovation lab topic. The strongest signal is adoption. As noted in this insurance GenAI report summary from Master of Code, 59% of insurance organizations have adopted generative AI, with reported outcomes including 61% staff productivity gains, 56% cost savings, and 50% shorter customer call times.

That matters because insurance executives rarely invest at scale on hype alone. They invest when a technology starts affecting claims cost, service expense, underwriting throughput, and retention pressure. Generative AI now sits in that category.

Why insurance reached this point faster than many sectors

Insurance has three conditions that make generative AI especially useful.

- The work is document-heavy: Claims files, submissions, policy schedules, broker emails, medical notes, repair estimates, and compliance language create constant reading and summarization work.

- The decisions are time-sensitive: Delays in claims, service, or underwriting raise operating cost and damage customer experience.

- The environment is regulated: Staff need answers tied to current policy language and approved internal guidance, not plausible-sounding guesses.

Those conditions make generative AI valuable when it helps people read faster, find the right source material, extract key facts, and draft first-pass outputs. They also make governance critical.

Practical rule: In insurance, the winning AI program usually starts by reducing reading, searching, and handoff time inside existing workflows.

Many executives still approach this as a use-case inventory exercise. That's too shallow. A better starting point is operational friction. Where do underwriters lose time reading submissions? Where do adjusters spend hours assembling file context? Where do service teams hunt across disconnected knowledge sources? That's where generative AI solutions in insurance usually justify themselves first.

For leaders looking at adoption patterns across carriers, AmasaTech's overview of AI adoption in insurance is useful context because it frames the move from experimentation to business-led deployment.

What separates momentum from theater

Teams make progress when they fund narrow, measurable deployments. They stall when they launch broad assistants without data discipline, process ownership, or a decision on where humans stay in control.

A credible insurance AI program has four traits from the start:

| Deployment trait | What it looks like in practice |

|---|---|

| Clear workflow target | One process, one owner, one measurable pain point |

| Grounded outputs | Responses tied to approved policies, files, or knowledge bases |

| Human accountability | Staff approve or override outputs at defined checkpoints |

| Measurement | Handling time, quality, routing accuracy, and adoption are tracked |

That's the tipping point. The firms moving now aren't asking what AI can theoretically do. They're deciding which workflows deserve production-grade treatment first.

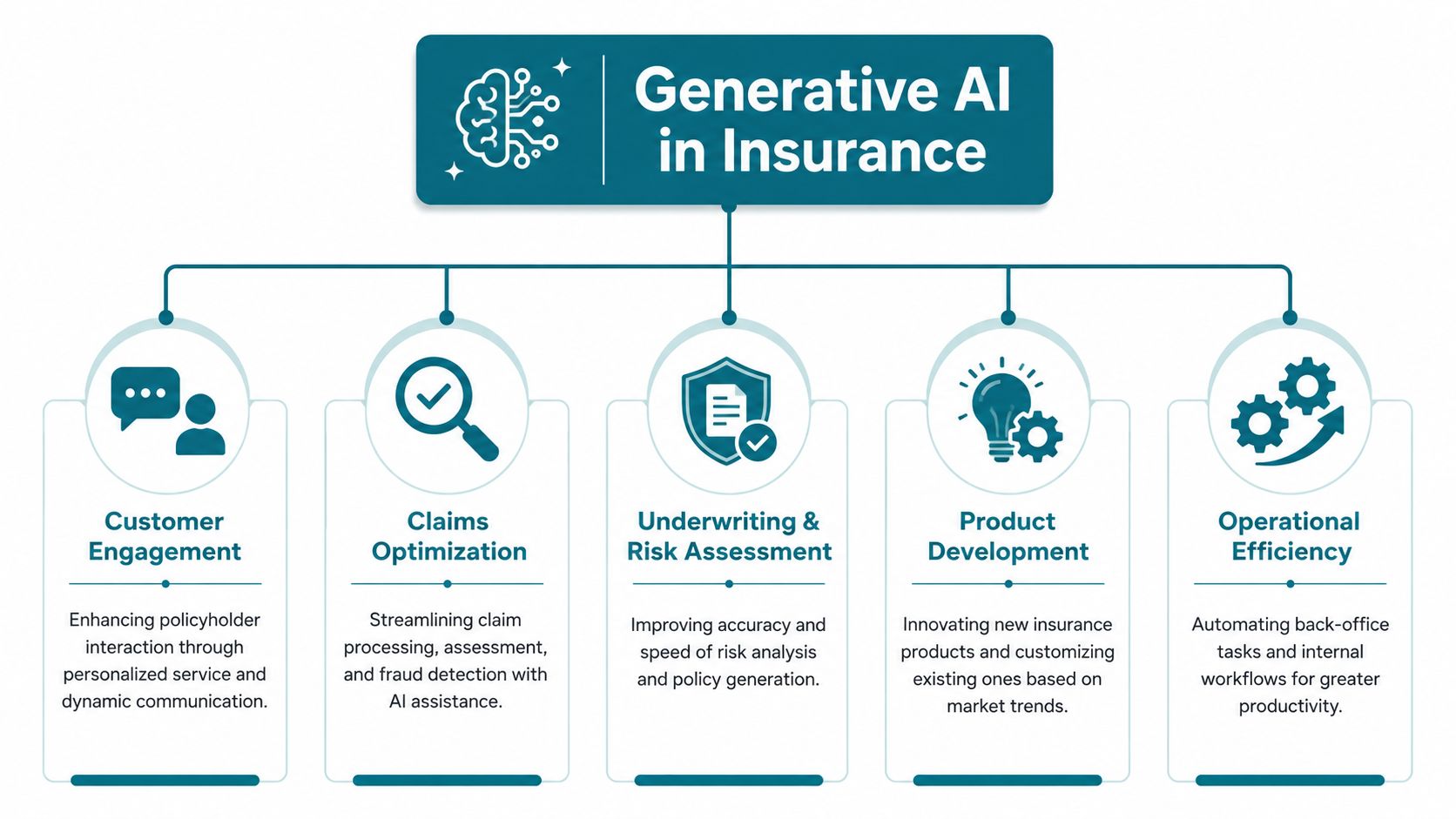

Core Generative AI Applications Transforming Insurance

The most useful way to evaluate generative AI solutions in insurance is to look at where the model removes manual reading, drafting, and context switching without taking final accountability away from trained staff.

Claims operations and file understanding

An adjuster receives a property claim with a first notice of loss, photos, repair documents, prior correspondence, and policy terms spread across multiple systems. The old process requires opening each item, building a mental timeline, identifying missing information, and drafting a next-action summary. A well-designed generative AI layer can assemble that context into a structured brief.

Production performance matters. According to Shift Technology's reported insurance GenAI results, deployments for document classification, key information extraction, and claims situation assessment have achieved 95–99% accuracy. The same source reports 90%+ accuracy in auto claims, 95% in property claims for liability assessment, and a 30% increase in subrogation referral acceptance when AI supports liability determination.

That doesn't mean the model should adjudicate claims alone. It means the system can do the first-pass reading, extraction, summarization, and routing work that slows teams down.

Underwriting support and submission review

Underwriting is another strong fit because submissions arrive incomplete, inconsistent, and buried in attachments. Generative AI can review broker emails, inspect narrative documents, identify missing items, summarize exposures, and prepare a clean brief for the underwriter.

The key word is augment. Strong systems don't replace underwriter judgment. They reduce low-value reading and make issues easier to spot. In practice, the tool should surface what was found, what is uncertain, and what source documents support the summary.

A useful pattern here is pairing extraction and summarization with document intelligence workflows built for operational review. That gives teams a way to convert unstructured insurance material into decision-ready inputs instead of another pile of text.

Customer service and knowledge assistance

Customer service teams often deal with repetitive but sensitive questions about coverage, billing, endorsements, claim status, and policy documents. Generic assistants tend to fail here because they answer too broadly. Knowledge-grounded assistants perform better when they retrieve approved answers and present them in plain language.

Service AI should be judged less by how conversational it sounds and more by whether it gives agents and customers the right answer from the right source.

Many insurers make an avoidable mistake: they launch an external chatbot before cleaning up internal knowledge access. In practice, internal service assistance usually creates value sooner because it improves agent performance while keeping a trained human in the loop.

Policy servicing and document generation

Generative models are also useful for drafting policy-related communications, summarizing endorsements, preparing renewal outreach, and translating technical insurance language into plain-English explanations for customers or staff. Drafting is a productive use case when the output is treated as a reviewed starting point.

A short comparison makes the trade-off clear:

| Use case | What works | What fails |

|---|---|---|

| Claims summaries | File-grounded summaries with source links | Open-ended summaries with no evidence trail |

| Underwriting briefs | Missing-data flags and source-backed extraction | Freeform risk recommendations with no rationale |

| Service support | Knowledge-grounded answers for agents | Public chatbot answers pulled from generic model memory |

| Document drafting | First-draft letters and explanations with review | Fully automated customer communications in sensitive cases |

Fraud and liability support

Generative AI doesn't replace fraud models, but it can help investigators and claims teams understand narrative inconsistencies across notes, statements, and supporting documents. It can also draft referral rationales and summarize why a case needs escalation.

The strongest insurance deployments are rarely flashy. They solve the repetitive cognitive work that consumes expert time. That's why the most practical generative AI solutions in insurance tend to sit inside claims, underwriting, service, and document workflows rather than outside them.

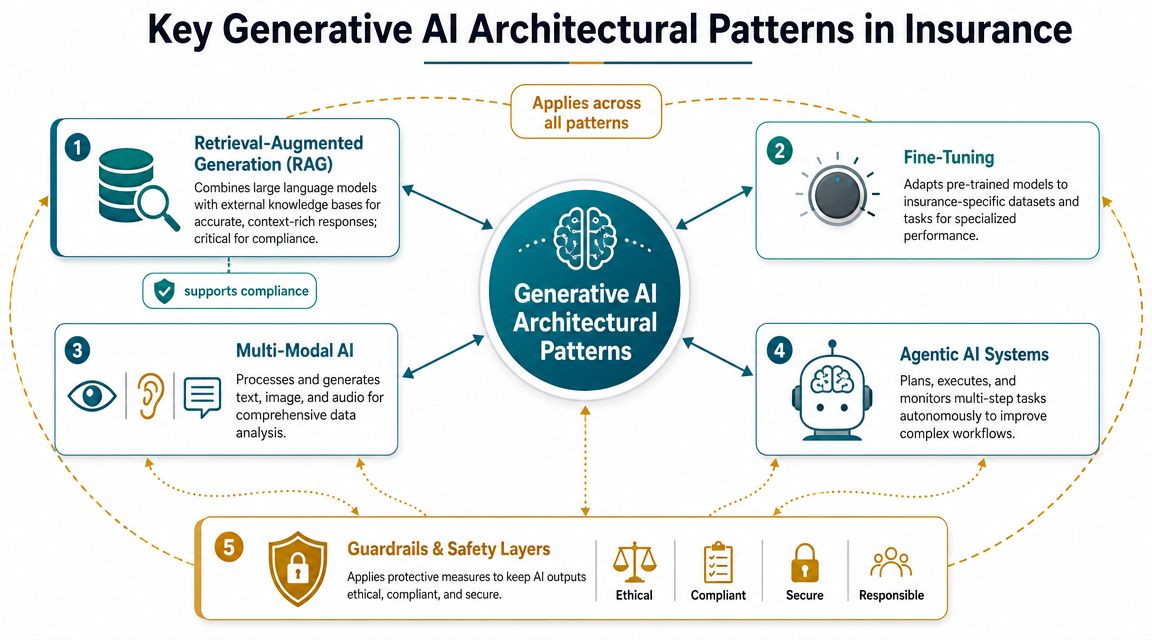

Understanding the Key Architectural Patterns

Insurance leaders don't need to become model architects. They do need to know which design choices affect compliance, accuracy, and total deployment risk.

Why RAG is the default architecture

The dominant pattern in insurance is retrieval-augmented generation, usually shortened to RAG. The simplest analogy is an open-book exam. Instead of asking a model to answer from memory, you first give it access to the right books, policies, claims documents, and approved internal guidance. Then you require the answer to stay grounded in those materials.

That's why Hexaware's write-up on insurance GenAI architecture points to RAG-backed document intelligence as the most effective technical pattern for insurance. It allows models to summarize case files, extract data from unstructured loss reports and broker emails, and draft decisions while grounding outputs in specific policy language.

For insurance, that grounding changes everything. It reduces hallucination risk, supports auditability, and makes human review much more practical.

When a plain LLM is the wrong tool

A generic model with no retrieval layer can still be useful for low-risk drafting. It's the wrong default for claims interpretation, coverage explanation, underwriting support, or regulated customer communication.

Here's the executive-level distinction:

- Plain LLM: Fast for generic writing tasks. Weak for controlled insurance decision support.

- RAG system: Better for policy-grounded answers, internal knowledge search, and file-based summarization.

- Fine-tuned model: Worth considering when a specific task has stable patterns and specialized language.

- Multimodal model: Useful when the workflow includes images, scanned forms, PDFs, or mixed media.

If your team is discussing architecture, this API architecture perspective from AmasaTech is relevant because production insurance systems usually depend on orchestration, retrieval, logging, and workflow integration more than on the model alone.

Where multimodal and agentic patterns fit

Insurance doesn't operate in text only. Claims often involve photos, scanned forms, repair documents, and handwritten notes. Multimodal systems can process mixed inputs and produce a coherent working summary for a claims team.

Agentic patterns are getting attention because they can coordinate multi-step tasks such as gathering documents, querying knowledge bases, drafting summaries, and routing the outcome. They're promising, but they need more control than many buyers expect. In insurance, agentic workflows should be narrow, observable, and constrained by rules, source access, and approval steps.

The model isn't the product. The product is the controlled system around the model.

The minimum production stack

A reliable insurance deployment usually includes these layers:

- Document and data ingestion for emails, PDFs, notes, and structured records.

- Retrieval and indexing so the model can access current approved content.

- Prompt and policy controls that shape how the model responds.

- Human review checkpoints for sensitive outputs.

- Logging and versioning so teams can inspect what happened later.

This is why architecture is a business decision, not just an engineering one. The wrong pattern creates operational risk. The right one makes AI usable in a regulated enterprise.

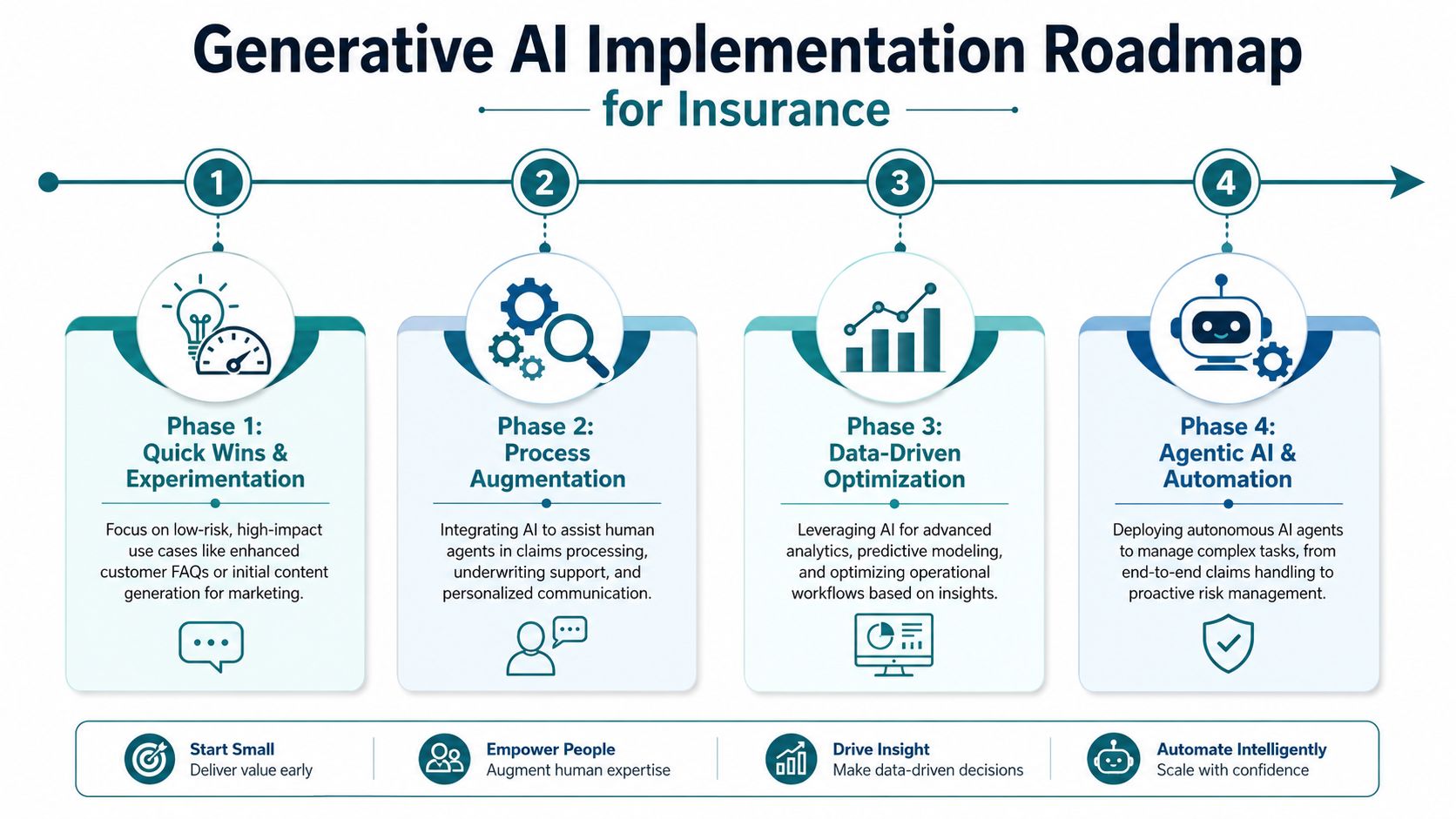

Your Implementation Roadmap Quick Wins to Agentic AI

The fastest way to lose executive support is to start with the most ambitious automation idea in the building. Insurance teams usually scale successfully when they move in phases and prove value before widening the scope.

Phase one starts with operational friction

The best early deployments target work that is frequent, manual, and low in decision risk. Bain's insurance analysis notes that successful enterprise deployments focus first on applications with measurable operational lift, such as RAG for internal knowledge search and multimodal models for claims assessment, instead of jumping straight to open-ended chatbots.

That aligns with what tends to work in practice:

- Internal knowledge assistants: Help service reps or adjusters find policy rules and process guidance faster.

- Claims file summarization: Turn long files into a structured case brief before human review.

- Submission intake support: Extract core details from underwriting packets and flag missing items.

These use cases create value because they improve how employees work before trying to automate full decisions.

Phase two integrates into core workflows

Once a team trusts the output quality and understands exception patterns, the next step is workflow integration. With this integration, AI starts showing up inside adjuster queues, underwriting workbenches, and service desktops.

A simple maturity view helps:

| Phase | Primary objective | Human role |

|---|---|---|

| Quick wins | Reduce search and reading time | Review and use suggestions |

| Process augmentation | Assist triage, drafting, and prioritization | Approve, edit, escalate |

| Optimization | Improve routing and handoffs across systems | Supervise exceptions |

| Agentic automation | Coordinate multi-step tasks | Control boundaries and sign-off |

At this stage, the work changes from “can the model do this?” to “can the process absorb this safely?” That usually means system integration, role-based access, approval paths, and better exception handling.

For teams planning further maturity, this view on agentic AI workflows is a useful reference for thinking about orchestration rather than just single prompts.

Phase three requires narrower ambition than most roadmaps suggest

Agentic AI is real, but many insurers aim too wide too early. The practical path is to assign agents to bounded tasks such as collecting required documents, checking whether all needed inputs are present, generating a first-pass summary, and routing the case to the right person.

That's a strong operating model because each step is observable and reversible. It also forces teams to define where autonomy ends.

Don't ask an agent to “handle claims.” Ask it to complete one controlled unit of work inside the claims process.

The strongest roadmap isn't the most aggressive one. It's the one that compounds trust. Quick wins create adoption. Integration creates advantage. Controlled agentic workflows create scale.

Navigating Risk Compliance and Data Governance

The biggest failure in insurance AI programs isn't usually model quality. It's weak governance dressed up as innovation.

Auditability has to exist before scale

Insurance leaders often ask whether a model is accurate enough. The tougher question is whether the organization can prove why a specific output was generated, which source material informed it, which prompt version was active, and who approved the result.

That's why ValueMomentum's commentary on GenAI risk in insurance highlights a core gap in many AI strategies: insurers must be able to prove a model's output is defensible and traceable to approved policy language or claims files for pricing, claims adjudication, and underwriting decisions.

If that evidence trail doesn't exist, the deployment isn't production-ready.

The controls that matter most

A workable governance model is less about policy statements and more about operational controls. These are the controls insurance executives should ask for:

- Source traceability: Every answer should show what documents or knowledge sources were used.

- Prompt and version control: Teams need a record of what instructions shaped the output at the time.

- Human escalation rules: Sensitive cases must move to a licensed or designated reviewer.

- Role-based access: The AI system shouldn't expose claims or policy data beyond approved permissions.

- Output logging: Teams need logs for review, dispute handling, and continuous improvement.

That's the difference between a demo and a governed system. If an insurer can't inspect the chain of evidence, it can't responsibly rely on the output.

Bias, privacy, and decision boundaries

Underwriting and claims are especially sensitive because biased or poorly explained outputs can create legal, regulatory, and reputational risk. For that reason, many insurers should limit generative AI to support tasks first, such as summarization, extraction, and draft preparation, while humans retain decision authority.

A practical governance checklist looks like this:

| Governance area | Executive question |

|---|---|

| Data privacy | What data enters the model and where is it processed? |

| Decision authority | Which outputs are suggestions only, and which can trigger action? |

| Explainability | Can staff see the evidence behind the answer? |

| Bias monitoring | How are teams checking for unfair patterns in outputs? |

| Operations | Who owns incidents, retraining decisions, and policy changes? |

For insurers building controls around regulated workflows, AmasaTech's insurance compliance automation work is one example of the kind of implementation pattern to examine. The important point isn't the vendor. It's the discipline: traceability, access control, review paths, and accountability need to be designed up front.

A model can summarize a claim file in seconds. That's useful. It doesn't remove the insurer's obligation to explain, defend, and govern the outcome.

Measuring Success and Selecting the Right Partner

Insurance executives don't need another AI experiment. They need a controlled investment case.

One reason this matters now is market direction. The generative AI in insurance market is projected to grow from USD 346.3 million in 2022 to over USD 5.5 billion by 2032, a 32.9% CAGR, according to Ideas2IT's summary of insurance GenAI market projections. That projection doesn't prove your program will work. It does show that competitors are likely building capability while many firms are still debating pilot scope.

Measure workflow outcomes, not model theater

Most insurance teams start with the wrong metrics. They track prompt quality or demo satisfaction instead of business movement inside the process.

A better scorecard asks:

- Claims operations: Are adjusters spending less time reading and preparing files?

- Underwriting: Are submissions being reviewed faster and more consistently?

- Service: Are teams resolving questions with fewer handoffs and less search effort?

- Operations: Is more unstructured information becoming usable inside workflows?

If a use case can't be connected to a measurable operational outcome, it probably shouldn't be funded yet.

A strong KPI in insurance is tied to a queue, a handoff, a review burden, or a decision delay.

What to look for in an implementation partner

Buying a model API is easy. Operationalizing generative AI solutions in insurance is not. The partner matters because the hard part sits in workflow design, retrieval quality, governance, integration, and change management.

Use this evaluation lens:

| Selection criterion | What good looks like |

|---|---|

| Insurance process understanding | They understand claims, underwriting, service, and compliance realities |

| Architecture discipline | They can explain retrieval, orchestration, logging, and controls clearly |

| Governance readiness | They design traceability and human oversight into the system |

| Integration capability | They can connect AI to document stores, core platforms, and user workflows |

| Outcome accountability | They define success in operational terms, not just technical delivery |

Vendor demos often overemphasize the model and underemphasize the operating design. Ask to see how they handle source grounding, exception management, role-based access, and post-launch monitoring. That's where production programs succeed or fail.

Don't outsource ownership

An external partner can accelerate delivery, but the insurer still needs internal ownership across operations, risk, legal, data, and technology. The strongest programs usually have one business owner per use case, one defined metric set, and one decision forum for governance.

That internal structure matters more than presentation polish. Without it, even strong technology ends up stuck between teams.

From Strategy to Scaled Impact

Generative AI in insurance has moved past the stage where a list of use cases is enough. The firms getting value are the ones treating it as an operating model decision. They start with painful workflows, choose architectures that keep outputs grounded, build human oversight into sensitive processes, and measure results in business terms.

That's the lesson behind enterprise deployment. The technology matters, but the sequence matters more. Start with narrow workflow wins. Build trust with grounded, reviewable outputs. Integrate into the daily tools that adjusters, underwriters, and service teams already use. Only then should you widen the scope toward more autonomous orchestration.

This is not optional. Insurance runs on documents, judgment, and compliance. Generative AI can improve all three when it's deployed with discipline. It can also create noise and risk when teams chase broad automation before they've solved governance, retrieval, and ownership.

Leaders don't need to bet the enterprise on one leap. They need a roadmap that funds the next credible step, proves value, and compounds learning. That's how generative AI solutions in insurance move from pilot decks to scaled impact.

If you're evaluating how to move from isolated GenAI experiments to a governed insurance AI program, AmasaTech works as an AI consulting partner that starts with an AI audit, builds phased roadmaps around measurable KPIs, and supports capabilities such as RAG pipelines, document intelligence, custom LLM apps, and agentic workflows in enterprise environments.