Revolutionize AP: AI Accounts Payable Services

Finance teams usually don’t decide to look at ai accounts payable services because the topic feels novel. They look because AP is straining the business.

Invoices arrive in multiple formats. Someone rekeys data into an ERP. Approvals sit in inboxes. Suppliers chase payment status. Controllers worry that duplicate invoices or policy exceptions will slip through. The team works hard, but the process still feels fragile.

That tipping point is where AI starts to matter. Not as a buzzword, but as an operating model change. The companies getting value from AI in AP aren’t just buying a dashboard. They’re redesigning how invoices are captured, validated, routed, approved, and audited so the finance team can handle growth without adding the same level of manual effort.

Beyond the Spreadsheet The Tipping Point for Manual AP

Monday starts with a familiar AP scramble. Ten invoices came through shared inboxes overnight. Three are scans from suppliers who still fax. Two need approval from managers who are traveling. One was already entered once, but no one is fully sure. By noon, the team is not doing finance work. They are triaging process gaps.

That pattern holds longer than many leaders expect, then fails all at once. A manual AP process can survive a certain invoice count, a certain number of entities, and a certain level of team familiarity. After that, small frictions turn into operating risk. Intake becomes inconsistent. Approval paths vary by person. Month-end closes with too many open questions about liabilities, exceptions, and payment timing.

The issue is not that spreadsheets are old. The issue is that spreadsheet-led AP depends on memory, side conversations, and heroic effort. That creates avoidable exposure: duplicate payments, missed early-payment terms, weak audit trails, coding inconsistencies, and supplier frustration when payment status is unclear.

What leaders usually notice first

- Approval lag: Invoices stall because ownership is unclear, escalation rules are informal, and approvers work from inboxes instead of a controlled workflow.

- Talent waste: AP analysts spend hours on data entry, three-way matching, and status chasing instead of handling exceptions, supplier communication, and controls.

- Scaling pain: A process that feels manageable in one entity often starts breaking across new geographies, acquisitions, or business units with different policies and ERP setups.

Practical rule: If AP performance depends on who happens to be available that day, the process will not scale cleanly.

This is also the point where founders and tech leaders can make a costly mistake. They buy an AP automation product before they define the operating model they need. In practice, the hard part is rarely invoice capture alone. It is fitting automation to your approval logic, ERP structure, exception handling, vendor master data, and control requirements.

A better starting point is to assess process maturity before choosing tools. This AI readiness checklist from AmasaTech helps teams review data quality, system dependencies, and workflow constraints so they can tell the difference between a quick software purchase and a workable implementation plan.

Why this is now a competitive issue

Manual AP slows more than invoice handling. It affects procurement coordination, cash visibility, supplier trust, and the finance team’s ability to support growth without adding headcount at the same rate.

For many companies, the right decision is not a full rip-and-replace. It is deciding which AP tasks should be automated, which exceptions still need human judgment, and whether standard software can fit the process you already have. If the answer is no, customization stops being a nice-to-have and becomes part of the business case.

The Core Engine of Modern AI Accounts Payable Services

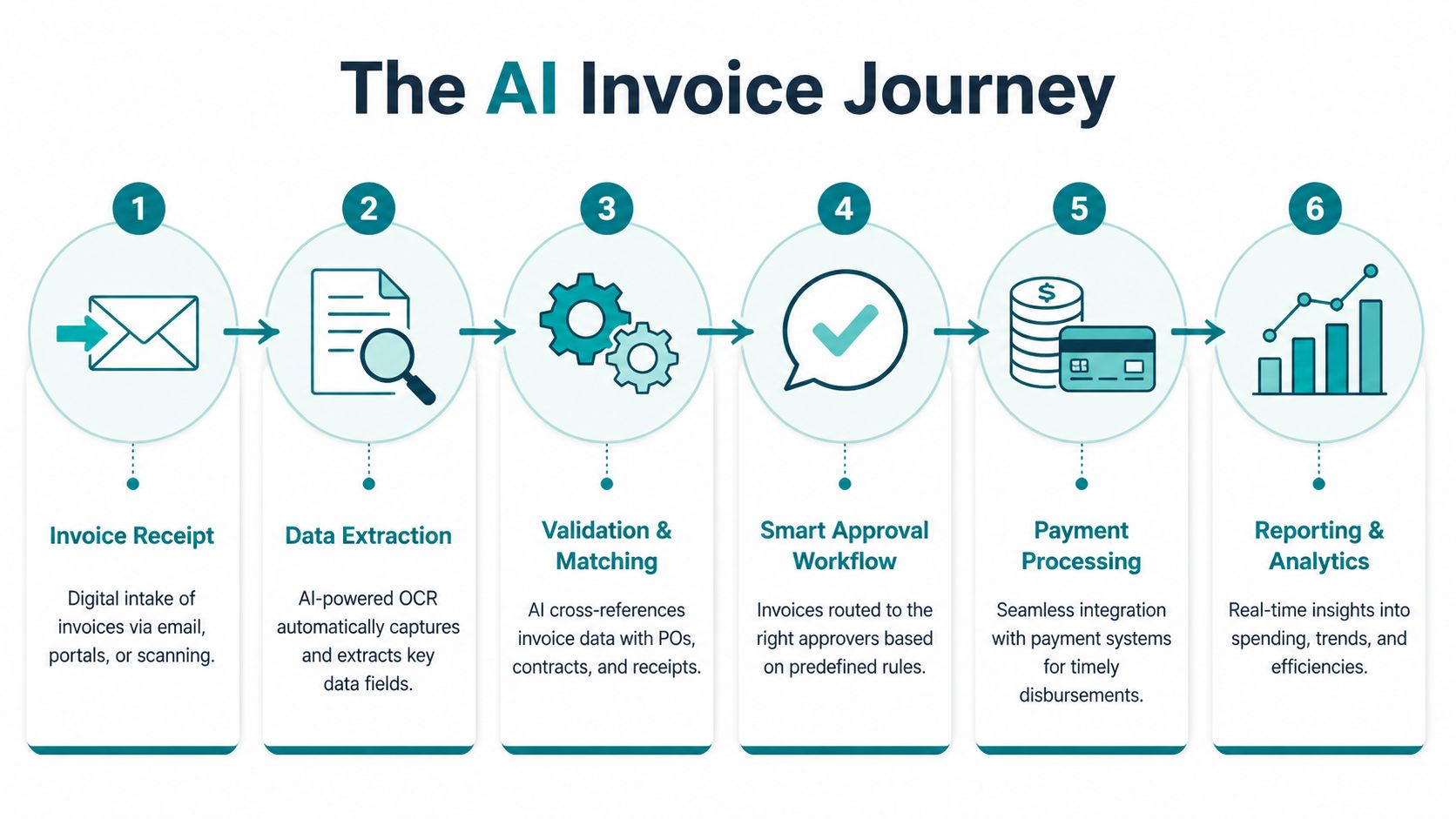

The best way to understand ai accounts payable services is to follow one invoice through the system. Good platforms act like a digital finance team. They ingest the document, read it, cross-check it against business records, route it, and surface only the cases that need a person.

Intake and extraction

The first job is collecting invoices from email, scans, portals, or uploads into a single intake flow. Basic OCR can read text, but AP usually needs more than text recognition. It needs usable finance data.

That’s where Intelligent Document Processing, or IDP, changes the equation. Unlike basic OCR, IDP uses AI and NLP to extract invoice metadata with extremely high accuracy, automating work that would otherwise take minutes of manual entry and enabling organizations to process payments up to 81% faster, as described in Serrala’s overview of AI in accounts payable.

If your organization handles invoices across multiple formats and layouts, this is the layer that usually determines whether automation holds up in practice. A strong document intelligence approach is what turns messy invoice inputs into structured data your ERP can trust.

Matching and validation

Extraction alone isn’t enough. AP systems have to determine whether the invoice should be paid.

That means checking core fields against the right business records. In PO-based environments, the system compares invoice values, line items, and supplier details against purchase orders and receipts. In non-PO scenarios, it may validate against contracts, historical patterns, or configured rules. AI proves particularly valuable, especially when invoice formats vary or coding patterns aren’t perfectly uniform.

A well-built workflow should do three things here:

- Accept clean invoices automatically when the match is clear.

- Flag exceptions precisely so humans review only the disputed fields, not the whole invoice.

- Learn from repeated decisions such as coding preferences, approver paths, and accepted vendor-specific patterns.

A practical AP AI system doesn’t aim to remove humans. It narrows human attention to the invoices that actually need judgment.

Workflow, payment, and analytics

Once validated, the invoice moves through approval. Good systems don’t just forward documents to a static list. They route based on policy, role, entity, spend type, and exception status. That’s a major difference between simple workflow automation and actual AI-enabled AP.

After approval, the payment layer connects into banking rails, treasury tools, or payment platforms. Then reporting closes the loop. Finance leaders can see pending liabilities, exception queues, approval bottlenecks, and vendor payment trends in near real time.

The technology stack varies. Some companies use platforms such as Coupa, Basware, Vic.ai, or Tipalti. Others combine a custom ingestion layer, an AI extraction service, workflow tooling, and ERP integrations. The right architecture depends less on feature checklists and more on how much of your AP process is standard versus unique.

Calculating the Business Impact and Financial ROI

A CFO approves an AP automation budget. Six months later, the team has faster invoice capture, but the finance lead still cannot say whether the project paid off. That usually happens when the business case was built around vendor features instead of the company’s actual AP workload.

The return from ai accounts payable services usually shows up in three areas: lower processing effort, better cash and liability visibility, and fewer control failures. The weighting is different in every company. A high-volume distributor may care most about invoice throughput. A multi-entity services firm may get more value from approval discipline and auditability. A company with frequent supplier changes may care most about fraud controls.

That is why I advise clients to model ROI from their current process first. Use your own invoice counts, exception rates, average approval time, duplicate-payment history, supplier inquiry volume, and audit remediation effort. If those inputs are weak, the ROI model will be weak too.

Where the business case usually becomes real

The first gains are operational, but they should be measured carefully. Reduced keying time matters. So does less rework on clean invoices, fewer inbox handoffs, and shorter approval lag. Those benefits often show up as capacity recovery before they show up as headcount reduction.

The next gains matter more than many initial spreadsheets assume. Finance gets earlier visibility into accrued liabilities. Controllers spend less time reconciling invoice status across email threads, ERP screens, and shared folders. Supplier conversations improve because AP can answer with current workflow data instead of manual status checks.

Risk reduction is the category buyers often undervalue.

AI can review payment behavior, invoice patterns, vendor changes, and approval anomalies at a scale manual teams cannot match. That matters because AP losses rarely begin as obvious fraud. They often start as a duplicate invoice that looks harmless, a bank-detail change processed too quickly, or an out-of-pattern payment that no one spots in time. Forrester’s review of top AI use cases for accounts payable automation in 2025 points to fraud detection as a high-value use case for AP automation.

For teams evaluating broader AI adoption strategies in financial services, AP is often a practical starting point because the process is repetitive, document-heavy, and tied to financial controls.

Manual AP vs AI-Powered AP A Comparison of Key Metrics

| Metric | Manual Process (Industry Average) | AI-Powered Process (Best-in-Class) |

|---|---|---|

| Processing cost per invoice | $12.88 | $2.78 |

| Approval cycle time | 17.4 days | 3.1 days |

| Touchless invoice processing | Average is lower than best-in-class | 49.2% |

As noted earlier in the article, industry benchmarks show a wide performance gap between manual AP teams and best-in-class automated operations. Those figures are useful for setting direction, but an internal business case should still be based on your process design, system constraints, and exception profile.

Key takeaway: The strongest AP ROI model includes labor savings, control improvements, and cash visibility. A model based only on headcount reduction usually understates the value and sets the wrong expectations.

A practical ROI model

A workable ROI model for AP AI should separate direct savings from harder-to-measure gains.

- Current-state cost: Manual invoice handling, exception rework, approval chasing, supplier status inquiries, and close-period cleanup.

- Avoided loss: Duplicate payments, fraud exposure, policy violations, missed discounts, and audit remediation effort.

- Strategic upside: Better liability forecasting, stronger supplier service, and finance capacity shifted from clerical work to review and analysis.

Build vs. buy decisions matter here too. An off-the-shelf platform can improve baseline metrics quickly if your AP flow is fairly standard. A custom or hybrid approach often produces better ROI when approval logic, entity structure, coding rules, or ERP integrations are unusual. The trade-off is a longer implementation path and more design work upfront.

Good ROI planning is less about proving that AI is valuable in general. It is about proving which version of the solution fits your AP operation, your controls, and your economics.

Your Implementation Roadmap and Integration Strategy

Most AP AI projects don’t fail because the concept is wrong. They fail because teams underestimate integration, data quality, and change management.

Up to 40-60% of AP AI projects fail due to poor data quality and legacy system incompatibility. For SMEs, the rate can be even higher, with many projects requiring a 12-18 month breakeven period and 25% needing custom development to succeed, according to Tipalti’s analysis of AI in accounts payable.

That’s the part vendors rarely emphasize. AI doesn’t erase process debt. It exposes it.

Start with process design, not model selection

Before choosing a platform or building custom components, map the actual AP flow. Not the policy version. The actual one.

Look at where invoices enter, how supplier records are maintained, who handles exceptions, how approvals really happen, and where payment data is updated. Teams that skip this step usually automate broken handoffs.

A solid preparation phase should include:

- Data cleanup: Supplier master records, PO references, coding histories, and duplicate records need attention before training or rule configuration.

- Exception mapping: Define which cases can auto-process and which must route to AP, procurement, finance, or legal.

- Ownership clarity: Someone must own data quality, workflow policy, and integration testing.

A practical preparation guide like preparing for AI adoption is useful because AP projects tend to sit across finance, IT, procurement, and operations.

Roll out in phases

The safest path is rarely a full AP replacement. It’s usually a phased rollout.

Start where invoice patterns are repetitive and policy rules are stable. Vendor invoices with consistent formats, clear PO matching, and known approval chains are better pilot candidates than edge-case spend. Once the system proves reliable there, expand into more complex categories.

Don’t measure a pilot by how much technology you deployed. Measure it by whether AP staff trust the outputs enough to change their daily behavior.

A phased model often looks like this:

- Pilot one intake lane such as a supplier group or business unit.

- Stabilize extraction and matching before pushing hard on touchless approvals.

- Expand exception handling rules only after the team agrees on ownership and escalation paths.

- Connect payments and reporting once upstream data quality holds.

Here’s a useful overview of how teams think about staged AI rollout in business environments:

Where custom work often pays off

Custom development becomes necessary when the AP process has unique approval logic, a heavily customized ERP, multi-entity routing, or supplier data spread across disconnected systems. In those cases, buying software still leaves a gap. Someone has to bridge it.

That’s why implementation strategy matters more than feature density. The best outcome often comes from combining a strong AP platform with selective custom layers for intake, orchestration, exception resolution, or reporting.

Evaluating Solutions and Choosing the Right Partner

The market for ai accounts payable services is crowded, and most products look similar in a demo. They all promise invoice capture, approvals, analytics, and faster processing. Key differences emerge after integration begins.

That’s where the build versus buy versus partner decision matters. You’re not only selecting software. You’re choosing how much of your AP capability will be standard, how much will be customized, and who will own the long-term system behavior.

What to ask before you buy

When evaluating solutions, note that only 10% of AP automation software features high-accuracy NLP, and only 15% offer adaptive AI-powered workflows. Also, 51% of CFOs in high-performing organizations are prioritizing these advanced tools for fraud detection and spend visibility, according to Planergy’s 2025 accounts payable review.

Those numbers matter because they explain why some AP systems feel intelligent and others feel like old workflow software with AI branding. Ask specific questions:

- How does extraction improve over time? If the answer is mostly template setup, the AI layer may be shallow.

- How are exceptions handled? Strong products isolate the disputed fields and preserve auditability.

- Can workflows adapt to entity, spend type, and historical behavior? Static routing becomes painful at scale.

- What happens with your ERP reality? NetSuite, SAP, Oracle, Microsoft Dynamics, QuickBooks, and custom finance stacks all create different integration demands.

Build, buy, or partner

A pure buy decision works when your AP process is mostly standard and your ERP environment is clean. In that case, a mature platform can accelerate value and reduce implementation burden.

A pure build decision makes sense when AP is tightly tied to custom internal systems, unusual controls, proprietary approval logic, or differentiated supplier operations. But building means you own model orchestration, maintenance, workflow reliability, and support debt.

A partner-led hybrid is often the most practical route. Use proven AP software or AI components where the market already solved the problem. Build custom layers only where your workflow, data model, or control model requires it.

Good AP architecture doesn’t maximize custom code. It places custom code where it creates leverage.

A practical scorecard

Use a weighted scorecard rather than a feature checklist. Review each option across:

| Decision area | What good looks like |

|---|---|

| Integration fit | Works with your ERP, payment systems, approval identity layer, and document sources |

| Workflow flexibility | Supports your real approval logic and exception ownership model |

| AI depth | Goes beyond OCR with NLP, learning behavior, and anomaly handling |

| Operational support | Clear implementation ownership, testing process, and post-launch optimization |

| Total cost of ownership | Includes customization, maintenance, retraining, and support effort |

That framework helps separate products that look polished from solutions that will survive contact with your finance operations.

Beyond Off-the-Shelf Partnering with AmasaTech for Custom AI Solutions

Off-the-shelf AP products can solve a real part of the problem. They usually don’t solve all of it. The gap is where many teams struggle. Legacy ERP constraints, entity-specific workflows, nonstandard approval logic, and fragmented supplier data rarely disappear just because a platform has AI features.

That’s why the most effective AP transformation work is often hybrid. Use packaged capabilities for standard functions. Add custom orchestration, data pipelines, business rules, and interfaces where your operating model differs. The objective isn’t to customize everything. It’s to customize the parts that create control, fit, and long-term advantage.

This is where a product-minded engineering partner matters. Teams need more than implementation support. They need architecture judgment. They need someone who can tell them when to configure, when to integrate, and when to build.

AmasaTech works in that middle ground. The company helps startups and enterprises design and develop AI-first systems that fit existing operations instead of forcing teams into generic workflows. If your AP future requires custom document pipelines, intelligent exception handling, ERP integration, or a broader finance automation roadmap, explore AmasaTech’s AI and software development services.

The strongest AP systems are rarely the most feature-heavy. They’re the ones that match the business well enough that people use them, trust them, and build on them.

Frequently Asked Questions about AI AP Services

1. What are ai accounts payable services?

AI accounts payable services use AI technologies to automate invoice intake, data extraction, validation, approval routing, exception handling, fraud checks, and reporting. Depending on the setup, this can be delivered through software, custom integrations, managed services, or a combination of all three.

2. How is AI AP different from traditional AP automation?

Traditional automation usually depends on fixed templates and rigid workflow rules. AI AP adds learning-based extraction, smarter exception handling, anomaly detection, and adaptive routing. In practice, that means fewer invoices need full manual review.

3. Should a startup buy AP software or build a custom solution?

Most startups shouldn’t build a full AP platform from scratch. They should buy standard capabilities where possible and build only the parts tied to unique workflows, data models, or product requirements. A hybrid approach usually keeps cost and complexity under control.

4. When does custom AP development make sense?

Custom work makes sense when your team has unusual approval logic, multiple entities, legacy systems that don’t integrate cleanly, or specialized controls that packaged tools can’t support well. It also makes sense when AP is part of a larger internal operations platform.

5. Can AI AP work with existing ERP or accounting software?

Yes, but compatibility is the primary issue. The question isn’t whether integration is possible. The question is how much custom work is required to make invoice data, approvals, vendor records, and payment status move reliably between systems. That’s why integration discovery should happen early.

6. What is Intelligent Document Processing in AP?

Intelligent Document Processing, or IDP, is the AI layer that reads invoices and converts unstructured documents into structured accounting data. It goes beyond basic OCR by handling fields such as supplier details, invoice amounts, PO references, and line items more effectively.

7. How long does AP AI implementation usually take?

The timeline depends on process complexity, data quality, and integration scope. A focused pilot can move quickly, while a multi-entity AP transformation with ERP customization takes longer. The safest approach is phased deployment rather than a big-bang rollout.

8. What are the biggest risks in AP AI adoption?

The most common risks are poor source data, unclear exception ownership, weak stakeholder alignment, and underestimating legacy integration work. Change management is also critical. If AP staff don’t trust the outputs, automation stalls even when the technology works.

9. Can AI help with AP fraud detection?

Yes. AI is well suited to pattern recognition across invoice and payment activity. It can flag duplicates, suspicious sequences, unusual vendor behavior, and payment anomalies for review. Human oversight still matters, but AI improves the quality and speed of detection.

10. What should I look for in an AP AI partner?

Look for integration depth, workflow design experience, strong document-processing capability, and a realistic implementation method. A good partner should also be willing to say when custom development is unnecessary. That’s usually a sign they’re optimizing for long-term fit, not project size.

If you’re planning an AP transformation and need a solution that fits your actual workflows, Amasa Tech can help you design, build, and integrate AI systems that create long-term operational advantage.