AI Adoption in Financial Services: Practical Guide 2026

Financial services spent $35 billion on AI in 2023 and is projected to reach $97 billion by 2027, according to RGP’s AI in financial services research. That single number changes the conversation. AI adoption in financial services isn’t a side experiment anymore. It’s becoming part of how firms underwrite risk, detect fraud, serve customers, automate operations, and defend margins.

The challenge isn’t deciding whether AI matters. It’s deciding where to start, how to govern it, and how to make sure the first initiative creates business value instead of becoming another stalled pilot. That’s where teams often struggle. They buy tools before they define outcomes, centralize models before fixing data quality, or launch copilots without changing how work gets done.

The firms getting this right tend to treat AI as an operating model change, not a software purchase. They choose narrow use cases with clear owners, build governance early, keep humans in the loop for material decisions, and invest in the people side as seriously as the technical stack. Teams that want to become AI-first in a practical way usually succeed when they connect AI directly to one of four goals: revenue growth, risk reduction, cost control, or speed.

Table of Contents

- The New Competitive Edge in Finance

- The Business Case for AI Adoption

- Key AI Use Cases Transforming Financial Services

- The Governance Imperative for Data Models and Risk

- Crafting Your AI Implementation Strategy

- Leading the Change with People Skills and Culture

- Tailored Roadmaps for Startups and Enterprises

- Frequently Asked Questions about AI in Financial Services

- What does ai adoption in financial services usually mean in practice

- What’s the difference between AI and machine learning in finance

- Is generative AI the best place to start for banks and fintechs

- How should a financial firm choose its first AI use case

- Can smaller firms adopt AI without building a large in-house team

- What usually causes AI initiatives to fail in financial services

- How important is human review in AI-driven financial workflows

- How long should firms stay in pilot mode

- What should executives ask before approving an AI project

The New Competitive Edge in Finance

AI has become a competitive edge in finance because it improves decisions where speed, pattern recognition, and consistency matter most. In lending, it helps surface signals earlier. In fraud operations, it spots suspicious behavior before static rules would. In service, it reduces waiting time while giving agents better context. In compliance, it handles repetitive review work that teams used to process manually.

That doesn’t mean every AI initiative creates value. Plenty don’t. The common failure pattern is straightforward. A leadership team approves an AI program because competitors are talking about it, a vendor demo looks impressive, and no one forces a hard discussion about workflow redesign, model monitoring, or who owns the output in production.

AI creates an advantage only when it’s attached to a business process that already matters and a team that can act on the output.

In practice, the strongest starting points in ai adoption in financial services usually share a few traits:

- High-volume workflow: The process runs often enough for automation or prediction to matter.

- Clear economic signal: The team can tie results to loss reduction, conversion, service quality, or processing speed.

- Available operational data: Not perfect data, but enough structured and usable information to train, test, or support models.

- Decision owner: Someone in risk, operations, product, fraud, or compliance will use the system and be accountable for results.

Large institutions and smaller fintechs approach this differently, but the underlying principle is the same. Don’t start with the most ambitious idea. Start with the operational bottleneck that drains time, creates errors, or slows customer response.

A good first initiative should feel slightly unglamorous. That’s often where the payoff is. The institutions that move fastest aren’t always the ones with the biggest budgets. They’re usually the ones that know exactly which process they want to improve and which trade-offs they’re willing to accept.

The Business Case for AI Adoption

AI earns a place in a finance budget when it improves a P&L line, lowers a controllable cost, or reduces a measurable risk. That is the standard executives should use. In financial services, the pressure is coming from all three directions at once.

Why the numbers matter

Spending is rising fast, and many institutions already report revenue and efficiency benefits from AI. As noted earlier, sector investment is projected to climb sharply, and firms are tying AI to growth, faster operations, and lower delivery costs in workflows such as onboarding and compliance.

The significance of those numbers is clear. AI has moved out of the innovation budget and into operating priorities.

For a first major initiative, I advise leadership teams to test the business case in three areas:

- Revenue expansion: Improve conversion, retention, pricing decisions, or service speed in customer-facing workflows.

- Operational efficiency: Cut manual review, reduce turnaround time, and contain headcount growth in functions with repetitive work.

- Risk mitigation: Lower fraud losses, improve monitoring, and catch exceptions earlier in processes where misses are expensive.

That framing is simple on purpose. It helps a startup decide whether a use case will extend runway, and it helps an enterprise decide whether a program deserves capital, compliance attention, and executive sponsorship.

A sound AI proposal should answer four questions before funding is approved. Which process changes. What metric improves. Who owns the result. What controls are required once the model is live. If those answers are vague, the projected ROI usually is too.

Where value shows up first

Early returns usually come from narrow workflows with clear baselines and obvious ownership. Onboarding, transaction monitoring, claims triage, service assistance, collections prioritization, internal knowledge retrieval, and document-heavy compliance work all fit that pattern because teams can measure cycle time, error rates, escalation volume, and loss exposure before and after deployment.

That is also why many firms bring in outside support before making platform decisions. A disciplined enterprise AI consulting approach helps leadership connect use cases to unit economics, governance requirements, operating model changes, and the internal skills needed to run AI in production.

The overlooked work starts after the model demo. Enterprises need model risk review, data lineage, access controls, auditability, and clear sign-off between business, compliance, risk, and technology. Startups have a different constraint. They often move faster but lack experienced AI product managers, data governance muscle, or enough in-house capacity to monitor drift and exceptions properly.

Practical rule: If a team can’t describe the current workflow, error rate, approval path, and owner, it isn’t ready for AI yet.

Change management is part of the business case, not a separate workstream. If frontline teams do not trust the output, they will build manual checks around it and erase the efficiency gain. If compliance cannot explain how decisions are made, deployment will slow down in review. If managers do not redesign roles, AI becomes another tool people work around instead of use.

Strong business cases are specific. This system helps this team make this decision faster, cheaper, or with fewer losses. That is the level of clarity that gets budgets approved and results adopted.

Key AI Use Cases Transforming Financial Services

AI creates value in financial services when it improves a live decision point, not when it produces an impressive demo. The strongest use cases sit inside high-volume workflows where speed, accuracy, and consistency affect losses, revenue, or headcount capacity. That is why the first question should be operational: which decisions need better prioritization, faster review, or earlier intervention?

Fraud detection and AML

Fraud is often the first production win because the economics are clear. Every missed event creates direct loss. Every false positive creates customer friction, manual review cost, or both.

AI improves fraud and AML operations by combining transaction history, device signals, behavioral patterns, network relationships, and case outcomes into a risk score that updates in real time. Rule engines still matter. In practice, the best systems layer machine learning onto existing controls so teams can adapt faster to new attack patterns without throwing away proven rules.

According to Statista’s financial services GenAI and AI adoption data, firms are reporting meaningful gains from AI in fraud detection, and banks expect material cost savings as these systems mature. The implementation challenge is less about choosing a model and more about setting thresholds, managing latency, and giving investigators queues they can work with. Teams building payment controls often look at architectures similar to real-time fraud detection for payment platforms because production performance depends on decision timing, alert design, and exception handling.

Credit underwriting and scoring

Underwriting is a strong AI use case when the goal is better triage and better data extraction, not blind automation. Lenders use models to classify documents, extract income and employment details, detect inconsistencies across applications, and route straightforward files away from expensive manual review.

This usually works best in stages. Start with the parts of the process that are hard to dispute and easy to measure, such as document intake, completeness checks, or identity matching. Then expand into decision support for risk assessment once the credit team, model risk team, and compliance group agree on explainability standards and override rules.

The trade-off is clear. A more predictive model may improve approval speed or portfolio performance, but if adverse action reasons are weak or review paths are unclear, legal and operational risk rises quickly.

Algorithmic trading and execution support

Capital markets firms have used machine learning for years, but current adoption is shifting toward decision support across the desk. Models can identify execution opportunities, flag unusual market behavior, summarize research, and help traders compare live conditions against expected patterns.

The control model matters as much as the model itself. Research models, execution models, and surveillance models should not share authority by accident. Mature teams define where automation stops, where human approval begins, and what evidence is logged for review.

Keep autonomy narrow in high-risk environments. Keep monitoring broad.

A short explainer is useful here:

Robo-advisory and wealth operations

Wealth management gets more near-term value from advisor productivity than from fully automated advice. AI can prepare meeting briefs, summarize household activity, draft follow-up notes, flag suitability concerns, and surface next-best actions based on portfolio events or service needs.

That matters because many wealth firms still run on fragmented systems and labor-heavy service models. If advisors spend less time searching, documenting, and reconciling, they get more time for client conversations and higher-value planning. Clients notice the difference even when the AI stays behind the scenes.

For digital advice, firms still need clear product boundaries. Investment suggestions, disclosures, suitability checks, and escalation paths all need defined ownership before launch.

Personalized customer experiences

Customer service is one of the fastest-growing AI applications in finance because it affects both cost to serve and customer retention. Firms are using generative AI for agent assist, virtual assistants, knowledge retrieval, and service workflows that require context across accounts, products, and prior interactions.

The practical value comes from reducing handle time while improving answer quality. A good system can summarize prior conversations, pull policy guidance into the agent desktop, gather missing information from customers, and route edge cases to the right team without creating another disconnected channel.

Use cases that tend to hold up in production include:

- Agent assist: Suggest responses, summarize previous interactions, and surface approved policy guidance during live conversations.

- Customer self-service: Answer routine questions, collect required information, and hand off exceptions with context.

- Context-based outreach: Customize product education, reminders, and service nudges based on customer behavior and account status.

- Internal knowledge retrieval: Help staff find procedures, forms, and policy answers across multiple systems.

The failure mode is common. Teams launch a polished assistant before they have clean knowledge sources, escalation rules, or monitoring for hallucinations. In regulated service environments, customer-facing AI should answer from approved content, record what it said, and hand off quickly when the request moves into advice, disputes, or eligibility decisions.

The Governance Imperative for Data Models and Risk

AI governance in finance isn’t a compliance side project. It’s the mechanism that keeps useful systems from becoming legal, operational, or reputational liabilities. The more material the use case, the less room there is for vague ownership and undocumented model behavior.

A lot of teams realize this late. They build a promising pilot, business users like it, and then risk, legal, or compliance asks basic questions no one can answer. Where did the training data come from? What version is in production? What happens when inputs drift? Who signs off on exceptions? If those answers aren’t ready, rollout slows down fast.

Data governance

Data governance starts with quality, lineage, access, privacy, and retention. In finance, even a well-performing model will fail operationally if upstream data is inconsistent or poorly controlled. Customer records differ across systems. Transaction labels aren’t standardized. Internal notes mix structured and unstructured information. That’s enough to distort outputs before anyone notices.

This matters even more because AI is now closely tied to compliance workflows. According to the World Economic Forum report on AI in financial services, AI can automate up to 70% of KYC data collection and reporting, helping cut compliance costs by 25% to 35%. That’s powerful, but only if the underlying data is complete, traceable, and permissioned appropriately.

Good data governance usually includes:

- Lineage controls: Teams can trace what data entered the model and where it originated.

- Access design: Sensitive data is restricted by role, not exposed broadly because a model team asked for convenience.

- Data quality checks: Missing fields, schema changes, and inconsistent labels are caught before they corrupt downstream outputs.

- Retention policy: Firms know what data is stored, for how long, and under what rules.

Model governance

Model governance is where many executive teams underestimate the work. It covers validation, explainability, performance monitoring, drift detection, threshold setting, fallback rules, and retirement criteria. In plain terms, it answers whether the model is trustworthy enough for the decision it supports.

Some use cases allow looser tolerance. A document summarizer for internal notes can be useful even if it occasionally needs correction. Credit decisions, sanctions alerts, and fraud blocks require much tighter controls.

The right question isn’t “Is the model accurate?” It’s “Is the model safe and useful enough for this exact decision?”

The same WEF analysis notes that advanced fraud detection models such as CNNs and RNNs can achieve over 95% precision, substantially outperforming older rule-based systems in complex detection settings. But high precision doesn’t remove the need for governance. It increases the need, because teams become more likely to trust the system and expand its use.

A practical AI legal consulting approach for startups is often helpful for younger firms that haven’t yet built internal controls around model documentation, contractual risk, and regulated workflow design.

Regulatory and compliance controls

Regulators are paying closer attention because AI is moving into material decisions and critical operations. Governance needs to cover not just what the model does, but also who approves it, how it’s monitored, and how incidents are escalated.

A working control structure usually includes a short list of mandatory artifacts:

| Control area | What leadership should require |

|---|---|

| Model inventory | A record of every model in use, its owner, version, purpose, and status |

| Approval workflow | Defined sign-off from business, risk, compliance, and technical owners |

| Monitoring plan | Rules for drift, threshold breaches, audit logs, and review cadence |

| Human override | Clear authority for when staff can intervene, reverse, or escalate |

| Incident response | A playbook for failed outputs, harmful recommendations, and data issues |

The strongest governance programs don’t try to stop AI adoption in financial services. They make it deployable.

Crafting Your AI Implementation Strategy

A workable implementation strategy has to survive contact with real systems, real teams, and real constraints. Legacy platforms won’t disappear because an AI roadmap exists. Data won’t clean itself. Business users won’t trust outputs because the vendor says they should. The strategy has to account for those realities from the start.

Architecture decisions that hold up in production

Most financial firms don’t need a single grand AI platform before they begin. They need a stable integration pattern. That usually means connecting models to the systems where work already happens: CRM, loan origination, payment processing, case management, document repositories, risk tools, and internal knowledge bases.

The architecture should answer five questions early:

- Where inference happens: In a secure cloud environment, inside an internal environment, or through a controlled external API.

- How data flows: Batch, near real time, or streaming.

- What gets logged: Inputs, outputs, confidence, user actions, overrides, and exceptions.

- How humans intervene: Review queues, approval gates, or escalation routing.

- What happens on failure: Fallback rules, safe defaults, and rollback paths.

For many firms, the best first design is narrow. Keep the AI system as a service layer that assists a workflow instead of trying to rebuild the whole workflow around the model. That makes testing easier and lowers operational risk.

A useful planning reference is preparing for AI adoption inside the organization, because readiness problems usually appear in interfaces, process ownership, and data stewardship long before they appear in the model itself.

Build buy or partner

This is one of the most important decisions in ai adoption in financial services, and the wrong answer creates expensive delays.

Build makes sense when the use case is strategically differentiated, the data is proprietary, and the firm has enough technical depth to maintain the stack. Fraud scoring, internal decision support, and domain-specific underwriting logic often fit this category.

Buy works when the problem is common, the workflow is standardized, and speed matters more than differentiation. Think OCR, generic copilots, document extraction, or workflow tooling with AI built in.

Partner is often the strongest path for firms that need custom implementation but don’t want to assemble every capability in-house. This is especially true when the business knows the workflow well but lacks AI engineering, MLOps, model governance, or integration capacity.

Here’s the practical comparison:

| Option | Best when | Main risk |

|---|---|---|

| Build | The use case is core to competitive advantage | Longer path to production and heavier internal maintenance |

| Buy | The problem is common and the vendor product is mature | Limited customization and potential workflow mismatch |

| Partner | You need custom delivery with external expertise | Success depends on partner quality and internal ownership clarity |

Don’t choose build because it sounds strategic. Choose it only if you’re prepared to own the system after launch.

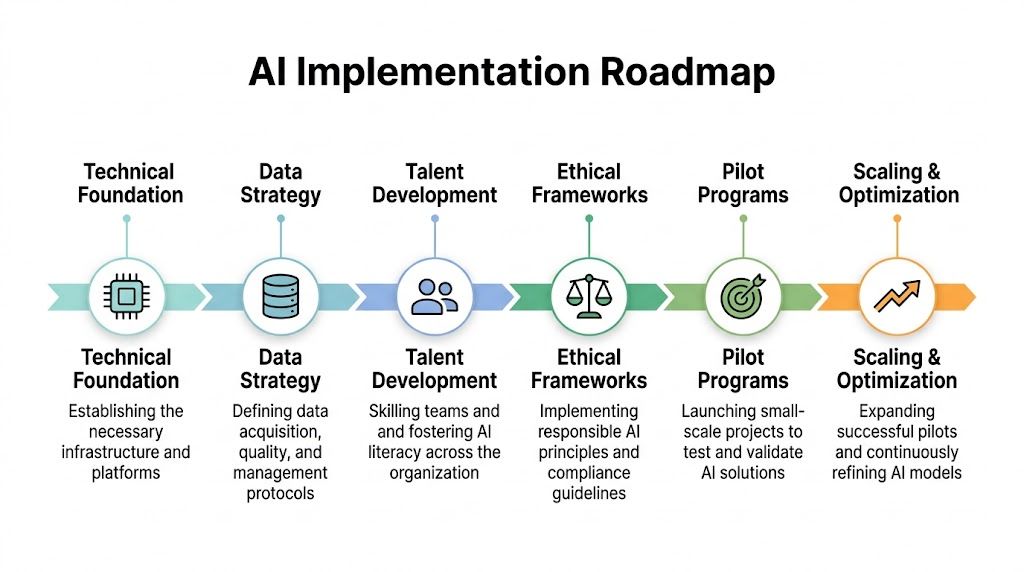

A phased roadmap that reduces risk

The best roadmap creates one useful production win before it tries to create enterprise transformation. That first win should prove business value, operational fit, and governance discipline.

A practical sequence looks like this:

Choose one process, not one technology

Start with a painful workflow such as onboarding review, fraud triage, service assistance, or document-heavy compliance work.Define the operating metric

Pick the metric that matters most to the owner. That could be review time, alert quality, queue reduction, approval turnaround, or manual effort.Set governance before launch

Decide what gets logged, who approves deployment, where human review sits, and what triggers rollback.Pilot inside a contained team

Use a small operational group with real data and real volume. Avoid sandbox-only pilots that never face production conditions.Review workflow impact, not just model output

Measure whether the process improved. A technically strong model that creates extra analyst work hasn’t succeeded.Scale by reuse

Reuse integration patterns, controls, monitoring, and review methods for the next use case instead of restarting from zero.

What doesn’t work is trying to roll out a broad AI mandate across customer service, risk, operations, and compliance at the same time. The organization becomes a coordination problem before the technology has proven itself.

Leading the Change with People Skills and Culture

Most AI programs slow down for human reasons, not technical ones. Teams don’t trust outputs. Managers can’t redesign roles. Risk and product operate on different timelines. Frontline staff sees automation as oversight instead of support. Those issues can stall a strong initiative even when the model works.

Why talent becomes the bottleneck

The talent gap in finance is larger than many executives expect. A 2025 Deloitte survey found that only 37% of financial services leaders with high AI expertise feel prepared in talent, dropping to 7% for followers, and many firms, especially SMEs, face 20% to 30% unreadiness in infrastructure and data, as summarized in CAF’s analysis on AI and financial inclusion.

That finding matters because it changes the implementation plan. If the organization doesn’t have enough data engineers, ML engineers, model risk specialists, product owners, and change leaders, the bottleneck won’t be the vendor or the budget. It will be execution capacity.

For SMEs and startups, this problem is sharper. They usually can’t build a full internal AI function quickly. For larger enterprises, the issue is different. They may have specialists, but those specialists are spread across silos and can’t move together.

What effective change management looks like

Strong change management in financial services is concrete. It doesn’t start with slogans about innovation. It starts with role-level clarity.

Teams need to know:

- What changes in daily work: Which tasks become automated, assisted, or escalated.

- What remains human-owned: Approval, exception handling, customer judgment, and regulated decisions.

- What new skills matter: Prompting, data interpretation, policy review, model monitoring, and workflow design.

- How performance will be judged: Staff shouldn’t fear being measured against a tool they weren’t trained to use.

A practical staffing model usually combines internal domain experts with external specialists during the first major initiative. Internal leaders know the process, constraints, and customer impact. External teams often bring implementation speed, model operations experience, and patterns from other deployments.

The cultural shift is just as important. Firms that succeed usually normalize review and iteration. They let teams question outputs, flag bad recommendations, and improve the system. Firms that fail often treat AI as something delivered to the business instead of something shaped with the business.

Adoption improves when people feel they are supervising a useful system, not being replaced by an opaque one.

Tailored Roadmaps for Startups and Enterprises

Startups and enterprises shouldn’t run the same AI playbook. Their constraints are different, their tolerance for complexity is different, and their path to value is different.

For a startup or SME, the best move is usually to focus on one customer-facing or operations-heavy workflow where speed creates an advantage. That might be onboarding assistance, service automation, fraud checks, or underwriting support. The goal is to ship something practical without building a large internal AI function too early.

Enterprises usually face the opposite problem. They already have pilots, fragmented tools, and overlapping stakeholders. Their work is less about getting started and more about deciding what to standardize, what to retire, and how to scale safely across business units.

Here’s a simple comparison.

AI Adoption Priorities: Startup vs. Enterprise

| Factor | Startup / SME Focus | Enterprise Focus |

|---|---|---|

| Primary goal | Reach usable business value quickly | Scale proven use cases across functions |

| Use case choice | Narrow, high-impact workflow with clear owner | Portfolio prioritization across multiple domains |

| Technology approach | Buy or partner first, build selectively | Blend internal platforms, vendors, and custom systems |

| Data challenge | Limited structure and smaller teams | Legacy silos, duplicated records, complex permissions |

| Governance style | Lightweight but disciplined controls from day one | Formal model risk, audit, compliance, and approval frameworks |

| Team model | Small cross-functional team with outside specialists | Federated teams with central standards |

| Biggest risk | Overbuilding before finding value | Pilot sprawl and inconsistent controls |

| Best starting point | One production use case tied to revenue, risk, or ops pain | One reusable pattern for deployment, monitoring, and governance |

The roadmap should fit the institution you are, not the institution you admire.

Frequently Asked Questions about AI in Financial Services

What does ai adoption in financial services usually mean in practice

It usually means deploying AI into a real business workflow, not just experimenting in a lab. Common examples include fraud detection, onboarding review, customer support assistance, document extraction, underwriting support, internal knowledge retrieval, and risk monitoring.

What’s the difference between AI and machine learning in finance

AI is the broader category. Machine learning is one way to build AI systems by learning patterns from data. In finance, teams often use machine learning for scoring, forecasting, detection, and prioritization, while broader AI systems may also include rules, orchestration, document processing, or generative interfaces.

Is generative AI the best place to start for banks and fintechs

Not always. Generative AI is useful for service, internal knowledge, summarization, and agent assistance. But many firms get faster business value from narrower predictive or automation use cases first, especially in fraud, operations, and compliance-heavy work. The right starting point depends on workflow pain, data quality, and governance readiness.

How should a financial firm choose its first AI use case

Pick a process that has four things: a visible business problem, a clear owner, usable data, and a realistic path to operational change. If the process is painful but no one owns it, or if the output won’t change a real decision, it’s a weak first candidate.

Can smaller firms adopt AI without building a large in-house team

Yes. Many smaller firms start by using existing platforms, targeted vendors, or implementation partners. The key is to keep ownership of the business process and controls internal even if parts of the technical delivery are external.

What usually causes AI initiatives to fail in financial services

The most common causes are poor data quality, unclear workflow ownership, missing governance, weak change management, and trying to launch too broadly. In many cases, the model isn’t the main problem. The operating design is.

How important is human review in AI-driven financial workflows

It’s critical for any material decision. Human review helps catch edge cases, handle exceptions, support explainability, and maintain accountability. The level of review should match the risk of the use case. A document summary needs less oversight than a credit or fraud action that affects a customer directly.

How long should firms stay in pilot mode

Not long. A pilot should prove operational usefulness, not delay decision-making. If a pilot can’t define success conditions, workflow ownership, and production controls, it’s not a pilot. It’s exploration. Exploration is fine, but leadership should label it transparently.

What should executives ask before approving an AI project

Ask five questions. What decision or workflow does it improve? Who owns the outcome? What data does it rely on? How will it be governed? What happens when it fails or produces a questionable output? If the team can’t answer those clearly, the project isn’t ready.

Amasa Tech helps startups and enterprises turn AI ambition into production-ready systems. If you’re planning your first serious AI initiative in financial services, Amasa Tech can help you define the right use case, build the product and data foundation, and deploy governed AI solutions that create long-term advantage.